Best health insurance plans USA 2026 – compare HMO, PPO, HDHP, costs & coverage. Tips to save money and pick the right plan for you.

Introduction

Alright… So let’s talk about health insurance. Yeah, I know—it’s one of those topics that makes most people’s eyes glaze over faster than a donut in a police drama. But trust me, if you live in the U.S., having a solid health insurance plan isn’t just “nice to have.” It’s a life-saver. Literally. Bills from hospitals can spiral out of control—been there, done that, and nope, I’m never doing it again.

Now, choosing the right plan feels overwhelming—so many terms, so many acronyms—HMO, PPO, EPO, HDHP… gah! But here’s the thing: it doesn’t have to be rocket science. This guide is going to break it down—plain and simple. I’ll walk you through what health insurance is, types of plans, how to pick the best one for you, plus tips to keep it affordable. And yeah, I’ll sprinkle in some personal stories, small quirks, and maybe even a “been there, totally freaked out” moment or two.

By the end of this article, you’ll actually feel confident making decisions—without needing a PhD in insurance jargon. So grab a cup of coffee—or tea, whatever fuels you—and let’s dive in.

What Is Health Insurance?

Okay, so first things first… what exactly is health insurance? At its core, it’s basically a safety net. You pay a monthly premium, and in exchange, your insurance helps cover medical costs when life throws a curveball—doctor visits, hospital stays, surgeries, prescriptions… the whole messy shebang.

Here’s how it usually works: think of your health insurance plan like a subscription—kinda like Netflix, but instead of movies, you get coverage. You pay your monthly fee (premium), then when you need care, you might pay a small part (copay) or a percentage (coinsurance). After you hit your yearly limit (deductible), the insurance often kicks in more heavily. Confusing at first, yes—but stick with me.

In the U.S., health insurance isn’t just “good to have”—it’s practically essential. Medical costs can skyrocket insanely fast. Imagine getting a surgery that costs $20,000… without insurance, you’re basically writing that check yourself. Ouch. Been there, and trust me, it’s not fun.

Also, there are different ways insurance works: some plans make you choose a primary doctor (HMO), some let you roam freely (PPO), and some are hybrids. There’s a lot of nuance, but the key takeaway is: insurance = protection + peace of mind. Plus, having it can sometimes save you money on preventive care—like screenings and vaccines—because insurers often cover those at little to no cost.

Now, I know what you’re thinking: “Okay, but which plan do I actually pick?” Hang tight, that’s coming up next… because the U.S. system is a bit of a maze, and navigating it without a map can leave you feeling like you’re wandering through IKEA with no exit signs.

Types of Health Insurance Plans in the USA

Alright… let’s break down the main types of plans, and I’ll try to keep it human-friendly because, honestly, this part can get real dry if we’re not careful.

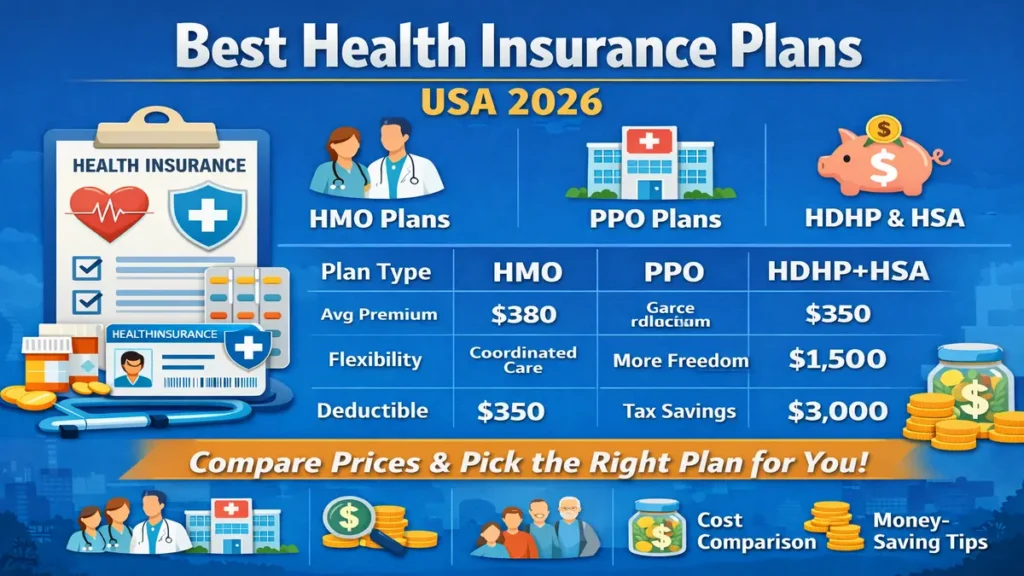

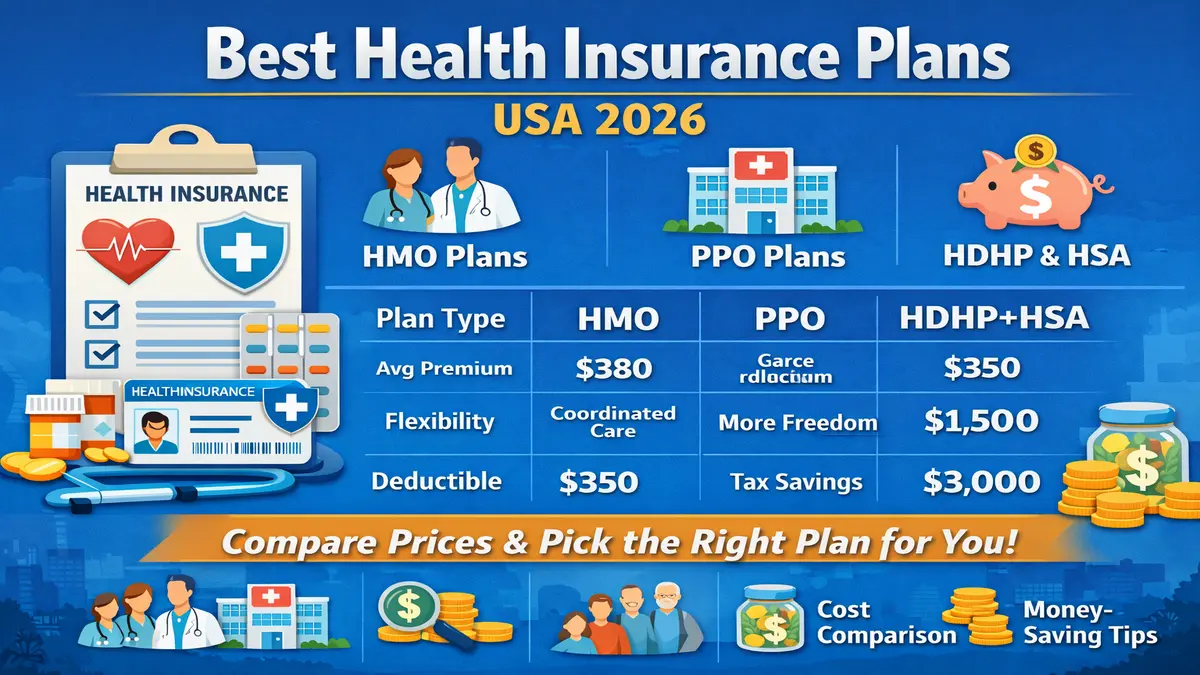

1. Health Maintenance Organization (HMO)

- You pick a primary care doctor (PCP) and usually need referrals to see specialists.

- Pros: Usually lower premiums, predictable costs, coordinated care.

- Cons: Less flexibility—you’re kinda “stuck” in-network.

- Personal note: I once had to wait a week for a referral to see a dermatologist… frustrating, but cheaper in the long run.

2. Preferred Provider Organization (PPO)

- More freedom—you can see specialists without referrals.

- Pros: Flexibility, wider provider network.

- Cons: Higher premiums, coinsurance can add up.

- Trust me… if you travel a lot or hate asking for referrals, this is your jam.

3. Exclusive Provider Organization (EPO)

- A hybrid—like a PPO but more network-restricted.

- Pros: No referrals, lower premium than PPO.

- Cons: Must stay in-network.

- Quirk: Sounds great, but if your favorite doctor isn’t in-network… tough luck.

4. High Deductible Health Plan (HDHP) + HSA

- High deductible, lower premiums. Often paired with Health Savings Accounts (HSA).

- Pros: Tax-advantaged savings, lower monthly payments.

- Cons: Pay more out-of-pocket before insurance kicks in.

- Been there… My first HDHP had me sweating at every doctor visit. But the HSA? Lifesaver.

5. Catastrophic Health Insurance

- For under 30s or certain hardship cases. Covers worst-case scenarios.

- Pros: Super low premiums.

- Cons: High out-of-pocket costs, minimal day-to-day coverage.

6. Medicare / Medicaid

- Medicare: federal program for 65+ or certain disabilities.

- Medicaid: state-based, income-dependent coverage.

- Pros: Affordable or free for eligible users.

- Cons: Eligibility varies by state, coverage gaps exist.

…So yeah, there’s a lot. But don’t freak out. Pick a type that fits your lifestyle, risk tolerance, and budget—then we’ll narrow it further with specific plans.

Comparison Table – Top Health Insurance Providers 2026

| Provider | Plan Type | Monthly Premium (avg) | Deductible | Network | Notable Feature |

| UnitedHealthcare | PPO | $450 | $1,500 | Nationwide | Wide specialist access |

| Blue Cross Blue Shield | HMO | $380 | $1,200 | State-based | Lower premiums, coordinated care |

| Cigna | PPO | $420 | $1,300 | Nationwide | Wellness programs & telehealth |

| Kaiser Permanente | HMO | $400 | $1,100 | Regional | Integrated care, top tech |

| Aetna | HDHP + HSA | $350 | $3,000 | Nationwide | HSA-compatible, flexible savings |

| Humana | EPO | $390 | $1,400 | Regional | Specialist access, no referrals |

Best Health Insurance Plans for Different Users

Okay, so you’re like… “Cool table, but which one’s actually for me?” Let’s break it down by user type.

1. Young Adults / Millennials

- Typically healthy, don’t visit doctors much.

- HDHP + HSA or Catastrophic plan can save big.

- Personal aside: I went HDHP at 27… felt like I was gambling every time I stubbed my toe. But the tax savings? Worth it.

2. Families / Parents

- Kids, checkups, vaccines, occasional ER visits.

- HMO or PPO works best—predictable costs, coordinated care.

- Tip: Look for pediatric coverage in-network. My niece’s ER visit once cost $200 with insurance—without it, that’s a nightmare.

3. Chronic Condition / Frequent Care Users

- Diabetes, heart conditions, recurring meds.

- PPO with lower deductible is usually ideal—less stress on frequent bills.

- Been there… monthly prescriptions can stack up fast. Insurance smooths that out.

4. Travelers / Remote Workers

- Need nationwide or international coverage.

- PPO or plans with large networks are key.

- Real talk: I once had to visit a specialist 500 miles away—thank goodness my PPO covered it.

5. Seniors (65+)

- Medicare + supplemental (Medigap) is typically best.

- Covers gaps, lowers out-of-pocket costs.

- My grandfather… without Medigap, one hospital stay would have eaten his savings. Scary stuff.

6. Budget-Conscious / Low-Income Users

- Medicaid if eligible, or subsidized ACA marketplace plans.

- Pro tip: check if your state offers extra subsidies—can save hundreds monthly.

…Basically, pick your lifestyle, budget, and health needs. It’s a puzzle, but once you know your “user type,” things get way clearer.

Related post

- Health Insurance in the USA 2026

- Car insurance in the USA — What It Covers, How Much It Costs, and How to Choose…

- Home Insurance in the USA — Coverage, Benefits, Costs & Complete Guide for Homeowners

- Pet insurance in the USA — Complete Guide for Pet Owners

- Health insurance in the United States

How to Choose Affordable Health Insurance

Alright… let’s talk about the part that keeps most people up at night: affordable health insurance. Because, let’s be honest, no one wants to spend half their paycheck on premiums—but at the same time, going cheap can backfire. Been there… I learned the hard way.

First thing: don’t just look at premiums. Yeah, low monthly payments are tempting—trust me, I get it—but you also have to check the deductible, coinsurance, and out-of-pocket max. I once picked a plan with a $200 monthly premium, thinking “score!”… until a minor surgery cost me more than $3,000. Ouch. Lesson: balance matters.

Next up: network matters. Make sure your preferred doctors, specialists, and local hospitals are in-network. Nothing worse than thinking you’re covered, then getting slammed with a surprise bill. Sounds weird, but I double-check the directory every year… just in case.

Another tip: look for subsidies or tax credits. If you qualify for ACA marketplace plans, you could save hundreds a month. I helped a friend recently apply for state subsidies—$250 saved per month! That adds up fast.

Also, consider Health Savings Accounts (HSAs) if you’re going HDHP. It’s like a secret little piggy bank for medical expenses—tax-free, rolls over, and you can actually grow it over time. Feels like magic.

Think long-term, not just short-term savings. Sometimes paying slightly higher premiums upfront saves thousands when emergencies happen. I used to be “premium-phobic,” but after a minor ER visit, I realized spending a little more monthly is peace-of-mind gold.

Finally… read the fine print. I know, I know, everyone hates it—but knowing what’s included, what’s not, and any hidden fees can save a ton of headaches. Micro pause moment: I once ignored coverage limits for medication. Big mistake. Lesson learned.

So basically, affordable insurance isn’t just the cheapest plan—it’s the one that fits your lifestyle, budget, and health needs while protecting you from unexpected disasters. Treat it like shopping for a car: low monthly cost doesn’t mean low overall cost.

Benefits of Health Insurance

Alright, let’s get real for a sec… why even bother with health insurance? I mean, sure, it costs money every month—but the benefits? Oh man, they’re worth their weight in gold.

First up: financial protection. Hospital bills are scary. Like… make-you-sweat-at-2AM scary. Trust me, I’ve seen a friend get slapped with a $15,000 emergency room bill just because he thought he was “healthy enough to skip insurance.” With coverage, that nightmare shrinks to something manageable—maybe a few hundred bucks. Huge relief.

Second: preventive care. Screenings, annual checkups, vaccines—they’re often covered for free. Crazy, right? It’s like the insurance company is nudging you, “Hey, stay healthy… we got your back.” I went for my yearly checkup recently and literally paid $0. Feels weirdly satisfying.

Then there’s peace of mind. Imagine not having to stress about what happens if you break a bone, get sick, or need surgery. That’s priceless. You can actually sleep at night without imagining worst-case scenarios.

Oh, and access to specialists. Need a cardiologist? Dermatologist? Without insurance, good luck. With it, you can see the right doctor without feeling like you’re robbing a bank.

Finally, support for chronic conditions. If you need ongoing medication or frequent visits, insurance keeps costs predictable. I had a friend with asthma—monthly meds were a breeze with the right plan, compared to paying out-of-pocket, which would have been… Well, let’s just say “not fun.”

So yeah… insurance isn’t just about emergencies. It’s about daily peace, small protections, and big safety nets. It’s like having a parachute, even when you’re just casually jumping off life’s little cliffs. Sounds weird, but I promise—it works.

Common Mistakes to Avoid When Choosing Health Insurance

Okay… let’s get real. Picking health insurance in the U.S. is tricky, and I’ve seen people (including myself, oof) make some classic mistakes. These slip-ups can cost hundreds or even thousands—so let’s talk about them.

1. Choosing Based on Premium Alone

Ah, the lure of a low monthly payment. I get it—“$250/month? Sold!” But here’s the catch: the deductible, coinsurance, and out-of-pocket max might be sky-high. I once went cheap, thinking I was saving money… ended up paying over $2,000 for a minor ER visit. Lesson learned: look at total potential cost, not just monthly premiums.

2. Ignoring the Network

Thinking, “My favorite doctor must be covered, right?” Wrong. Check the in-network providers. Out-of-network bills can be brutal. Micro-pause moment: I assumed my dermatologist was in-network… surprise $400 bill. Not fun.

3. Overlooking Deductibles and Coinsurance

Your deductible is the amount you pay before insurance steps in. Coinsurance is what you pay afterward. Small numbers seem harmless until you actually need care—then, bam, money flying out of your wallet. Trust me… math matters.

4. Forgetting About Subsidies or Tax Credits

Some people assume they “make too much” for help—but many qualify for ACA subsidies. I once helped a friend save $250/month just by applying. That’s nearly $3,000 a year—just by checking eligibility!

5. Neglecting Preventive Care Benefits

Preventive screenings, vaccines, and checkups are often free. People skip insurance thinking they’re healthy… then ignore small problems until they become big, expensive ones. Don’t do it. Been there, too.

6. Not Reviewing the Plan Annually

Your life changes—maybe a baby, a new job, moving states. If you don’t check your plan each year, coverage gaps or better options can slip by unnoticed. I’ve caught a few changes just in time, avoiding unnecessary bills.

7. Assuming All Plans Cover Everything

Nope. Not all medications or procedures are fully covered. Read the fine print, check your prescription formulary, and verify any special treatments. Weirdly tedious, but way cheaper than a surprise bill later.

Pro Tip: Treat insurance like shopping for groceries—but for your health. Look at the full picture, check the “ingredients” (coverage details), compare options, and don’t just grab the cheapest “box” on the shelf.

FAQs About Best Health Insurance Plans USA 2026

Alright… so I know health insurance can feel like a foreign language sometimes. I mean, HMO, PPO, deductible, coinsurance… it’s enough to make your head spin. But hey, I’ve been there. Let’s tackle the most common questions—no boring lecture vibes, promise.

Q1: Can I change my health insurance anytime?

Well… usually no. Most plans only let you switch during open enrollment—like a specific window each year—or if you have a qualifying life event. Think marriage, having a baby, losing a job, or moving states. I once missed open enrollment and had to wait an entire year… lesson learned, don’t procrastinate!

Q2: What’s a deductible anyway?

Okay, picture this: your deductible is the amount you pay out-of-pocket before insurance starts helping. So, if your deductible is $1,500, you pay the first $1,500 of bills. After that, your insurance starts covering a bigger chunk. It sounds scary, but knowing the number upfront helps.

Q3: HMO vs. PPO—which should I pick?

- HMO: cheaper premiums, referrals needed. Great if you like structure.

- PPO: higher premiums, more freedom to see specialists without a referral. Perfect if you travel a lot or hate asking for permission.

Personally? I started HMO, hated the referrals, switched to PPO… never looked back.

Q4: Are telehealth visits covered?

Yes! And thank goodness. I once had a midnight panic about a rash, and a virtual doctor visit saved me a trip to the ER. Some plans even cover video therapy sessions—mind-blowing convenience.

Q5: How do I know if my doctor is in-network?

Check the insurer’s provider directory online. Sounds simple, but double-check—sometimes listings are outdated. Been there… I thought my favorite dermatologist was in-network… surprise bill incoming. Ouch.

Q6: Is preventive care free?

Usually, yes! Annual checkups, vaccines, and screenings are often covered 100% thanks to ACA rules. Feels weirdly luxurious to get care and pay $0… trust me, I still double-check my bills out of habit.

Q7: What’s coinsurance?

Coinsurance is the percentage you pay after hitting your deductible. Example: if it’s 20% and a $1,000 procedure happens, you pay $200. Easy math, but can sneak up on you if you’re not tracking it.

Q8: Can I use my insurance abroad?

Usually not… unless your plan has international coverage or add-ons. I learned this the hard way on a trip to Mexico. Ended up paying out-of-pocket for a minor ER visit—fun story, terrible bill.

Q9: What’s the best plan for families?

Honestly, HMO or PPO with low deductibles and in-network pediatricians. My friend’s kid had a minor ER visit—covered beautifully. Predictable costs = happy parents.

Q10: How can I avoid surprise bills?

- Always stick in-network.

- Confirm costs with providers before procedures.

- Track deductibles and out-of-pocket max.

- And… I know it sounds annoying, but reading the fine print really saves you later.

So yeah… it might feel overwhelming at first. But with the right info, a little planning, and maybe a spreadsheet or two, you can navigate it without losing your mind—or your wallet.

Conclusion

So… we made it. Health insurance in the USA might seem like a maze, but it doesn’t have to be a horror story. By knowing the types of plans, understanding your needs, and picking the right provider, you can protect your health—and your wallet.

Honestly, it’s about peace of mind. I’ve been burned by skipping insurance. Bills stacked up, stress skyrocketed… never again. Now, with the right plan, I feel safer, smarter, and yes—slightly smug about my HSA.

Remember, there’s no perfect plan. But the “right” plan for you exists. Take your time, read fine print, ask questions, and trust your gut.